Choosing The Right Investment Account

Jul 16, 2026

When it comes to investing, one of the most important decisions you'll make is choosing the right type of account. Why? Because where you place your money can have a significant impact on how much you keep over time, thanks to different tax treatments, contribution limits, and withdrawal rules. Choosing the right account for you means aligning your financial goals—whether they're short-term or long-term—with the account that provides the best tax advantages and flexibility.

Let's break down the different types of investment accounts available today, many of which have been around for decades:

- Traditional 401(k): Offered by employers, this account lets you contribute pre-tax dollars, lowering your taxable income. The money grows tax-deferred, but you pay income taxes when you withdraw in retirement.

- Roth 401(k): Like a traditional 401(k), but contributions are made with after-tax dollars. Your money grows tax-free, and withdrawals in retirement aren't taxed.

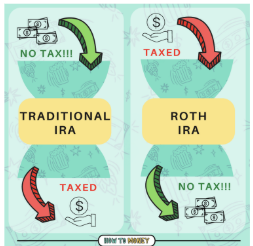

- Traditional IRA: A personal retirement account where contributions may be tax-deductible, with growth tax-deferred until withdrawal.

- Roth IRA: Contributions are made with after-tax dollars, and qualified withdrawals in retirement are tax-free.

- No Individual Investment Account (IRA): A taxable account with no contribution limits or restrictions. You can invest as much as you want, but you'll pay taxes on any dividends or capital gains each year.

- Joint Investment Account: Similar to an individual account but shared between two people, typically used by spouses or partners to manage joint investments.

Each account has its benefits and drawbacks, and the right choice depends on your financial strategy:

- 401(k) (Traditional vs. Roth): Traditional 401(k)s offer an immediate tax break and are ideal if you expect to be in a lower tax bracket during retirement. Roth 401(k)s, on the other hand, are bold bets on the future—tax-free withdrawals can be a huge advantage if you expect your income or tax rate to rise over time.

- IRAs (Traditional vs. Roth): A Traditional IRA gives you tax benefits today, but remember—you're deferring income taxes until retirement. A Roth IRA is bold because you pay taxes upfront, but it offers the reward of tax-free growth and withdrawals.

- Individual and Joint Accounts: These are the wild cards of the investment world. With no contribution limits, you can invest freely. However, the downside is that you pay taxes every year on any gains, which can eat into your returns. But if flexibility is what you need—whether for buying a house or managing other financial goals—they can be invaluable.

Stay in the Loop

Continue on your learning journey with our weekly newsletter!

You’ll also be the first to hear about updates on our book launch,

free resources, and you'll get early access to our courses!

We hate SPAM. We will never sell your information, for any reason.